Below is a PDF from my presentation at the May 16, 2013 event in the EU Parliament on the Economic Crisis and Access to Medicines in Europe. While the main purpose of my talk was to discuss delinkage, I began with some data on the EU market and R&D outlays. I have pulled out one figure and two tables from the presentation and offer some comments here.

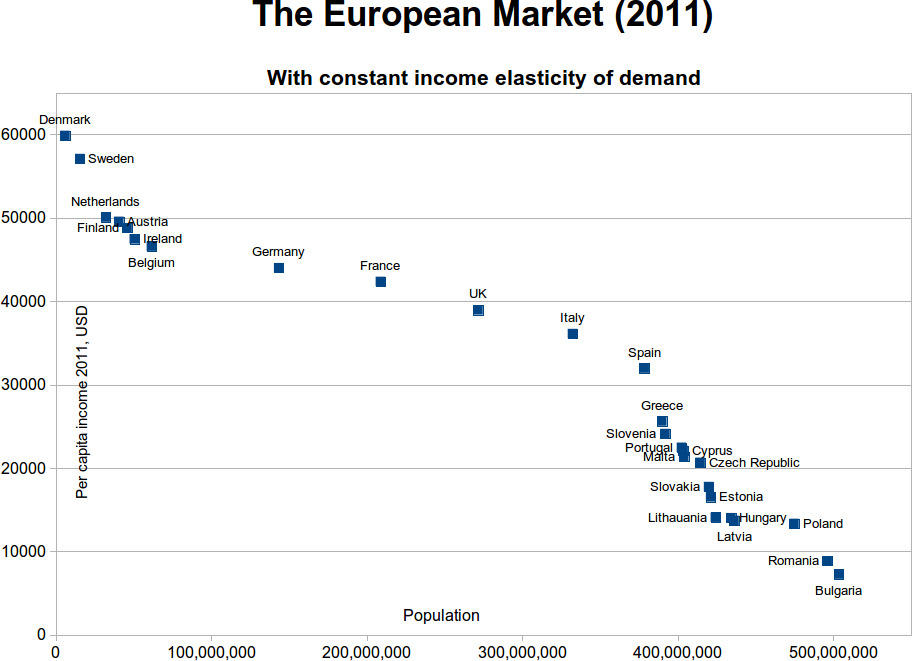

The figure below simulates the shape of the demand curve for Europe, if one assumes a constant elasticity of income for products, and insurance in each market.

Countries on the left of this demand curve will find the system to be working better than countries on the right.

The problems with price controls will be made more difficult by exclusions of persons from insurance, and the practical barriers to price segmentation in the EU market.

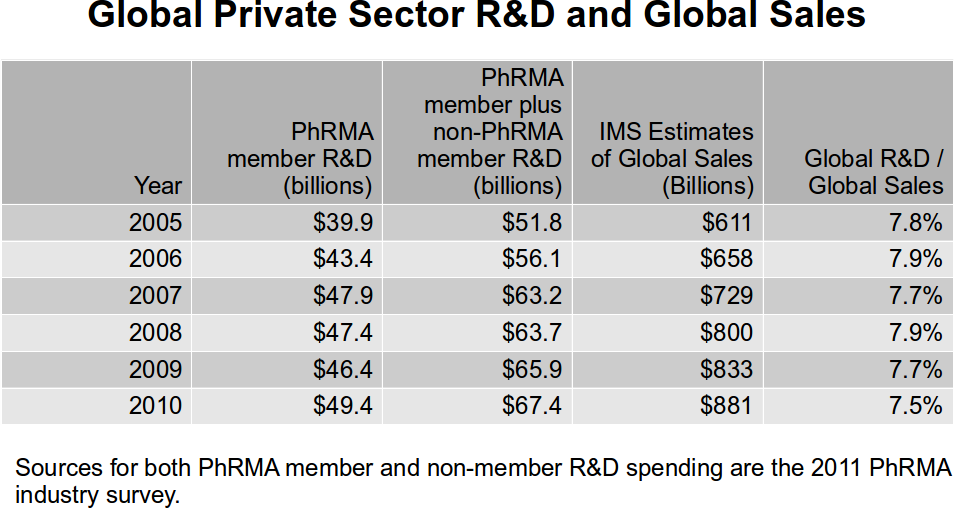

The second is a table that reports the global R&D and the global sales for pharmaceutical products from 2005 to 2010. Note that in no year were global private sector R&D outlays more than 8 percent of global sales.

Making the R&D outlays even less impressive as a percent of sales is the fact that at least half of the outlays are spent on projects of little or no medical benefit.

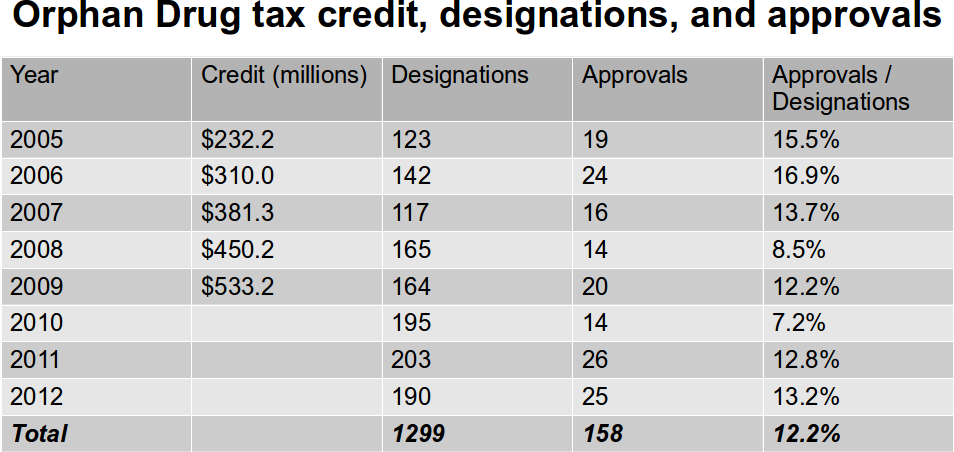

The next table provides some data from the US Orphan Drug program. It shows that from 2005 to 2012, the FDA made 1299 Orphan Designations, and during this same time, approved 158 orphan designations for marketing — a crude success rate of 12.2 percent for products that may have entered clinical testing. In other words, roughly one in eight Orphan products that enter clinical testing is approved for marketing.*

Note also that in 2009, the last year of the tax credit data, the combined US tax credit subsidy for clinical trials on orphan products was $533.2 million. Since the the tax credit covers 50 percent of the qualifying costs of trials, this is also a first approximation for private sector outlays for the same products. Note that the 50 percent credit was only $3.25 million per designation, or $26.7 million per approved designation, in the same year.

Notes

* The estimate is crude because some products enter testing without a formal FDA orphan designation, and some that receive orphan designations do not enter testing. Also, there is always a delay between receiving the designation and receiving marketing authorization, so the time periods are not a perfect match.